AW25/26 Knitted Scarf Trends: Colors, Yarns, and Silhouettes

AW25/26 Knitted Scarf Trends: Colors, Yarns, and Silhouettes

Trend forecasts are written by people who attend fashion weeks. Factory order books are written by buyers who place purchase orders. The two don't always agree. This article is based on the latter — the colors, yarns, and silhouettes that buyers are actually committing money to for Autumn-Winter 2025/26 delivery.

If you're sourcing scarves for AW25/26, here's what your competitors are ordering right now.

Color: What's Moving

The Core Palette — Safe Bets for Any Brand

| Color Family | Specific Shades | Demand Level | Fiber Pairing |

|---|---|---|---|

| Warm Neutrals | Camel, Oatmeal, Toast, Warm Greige | Very High | Wool, Cashmere, Alpaca blends |

| Deep Greens | Olive, Forest, Moss, Dark Sage | High | Wool, Cotton blends |

| Muted Blues | Ink Navy, Slate Blue, Dusty Periwinkle | High | Cashmere, Merino |

| Rich Reds | Burgundy, Oxblood, Rust | Moderate-High | Wool, Cashmere |

| Soft Pinks | Dusty Rose, Mauve, Blush | Rising | Cashmere, Mohair blends |

Camel and oatmeal are dominating across all fiber categories — they're the new black for winter scarves. A camel-colored cashmere scarf will sell. Period. Buyers who want to take less risk on color are leaning hard into warm neutrals and deep greens.

The "Differentiator" Colors — Higher Risk, Higher Reward

| Color | Risk Level | Who's Ordering It |

|---|---|---|

| Burnt Orange / Terracotta | Medium | DTC brands targeting design-conscious 25–35 demographic |

| Lavender / Soft Lilac | Medium-High | Korean and Japanese market buyers; gender-neutral brands |

| Chocolate Brown | Low-Medium | European heritage brands returning to 90s palette |

| Bright Cobalt | High | Streetwear brands, limited drops |

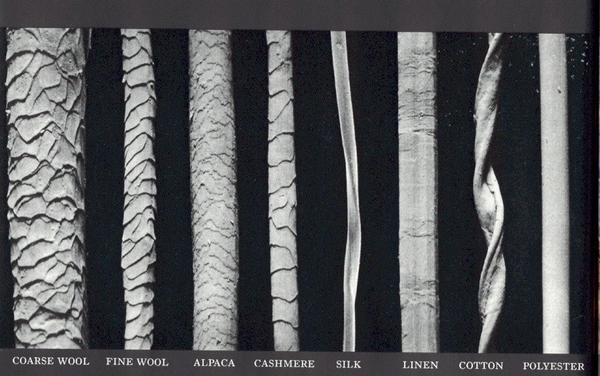

Yarn: What Buyers Are Specifying

Fiber Trends

| Trend | Direction | What It Means for Sourcing |

|---|---|---|

| Cashmere demand | Stable to slightly up | Grade A supply tight; expect Q3 price increases. Lock prices early. |

| Merino wool | Up — replacing lambswool in mid-tier | Buyers are upgrading from lambswool to merino as the mid-tier baseline. Lambswool is being pushed down to entry-level. |

| Alpaca blends | Up sharply | Alpaca-wool and alpaca-acrylic blends are the surprise growth category this season. Softer than wool, cheaper than cashmere. Lead times on alpaca yarn are extending. |

| Mohair | Niche but growing | Primarily in brushed finishes for a fluffy, halo-heavy look. High price point. Limited supplier base. |

| Recycled fibers | Rising steadily | Recycled wool and recycled polyester are being specified by EU brands under ESG mandates. GRS certification is becoming a minimum requirement for these orders. |

Yarn Weight Trends

The lightweight trend from SS25 is bleeding into AW25/26. Buyers are ordering finer gauges even for winter scarves. A 2/28 Nm that used to be standard for mid-weight is being pushed to 2/32 Nm and 2/36 Nm in some programs. The reason: consumers want scarves they can wear indoors as well as outdoors. A 400g chunky scarf is a coat replacement; a 250g fine-gauge scarf is an accessory.

This shift toward finer yarns increases spinning cost per kilo (finer yarn = more twist per meter = slower production) but reduces total yarn cost per scarf (less weight). Net effect: roughly neutral on total cost, but the scarf feels more refined at the same price point.

Silhouette & Structure: What Shapes Are Selling

| Silhouette | Trend | Dimensions | Who's Buying |

|---|---|---|---|

| Classic long scarf | Stable — still the volume leader | 180–200 × 30–35 cm | All markets |

| Oversized wrap | Growing | 200–220 × 50–60 cm | Premium brands, EU market |

| Square scarf (knitted) | Niche, stable | 80–100 × 80–100 cm | Japanese market; luxury brands |

| Skinny scarf | Declining | 160–180 × 15–20 cm | Fading trend; don't over-order |

Knit Structure Preferences

- Rib stitch (1×1, 2×2): Dominant. Buyers like the stretch recovery and the vertical visual line.

- Jersey (stockinette): Stable. The default for printed scarves because it provides a smooth surface.

- Cable knit: Resurging. Heritage and outdoor brands are bringing back chunky cable patterns as a point of differentiation.

- Fisherman's rib / half-cardigan: Growing in premium. Thicker, spongier, more luxurious hand feel at the cost of higher gram weight.

- Jacquard / intarsia: Rising for brand logos and geometric patterns. Adds $0.30–$0.80 per piece in knitting complexity.

What's Not Working: Trends to Avoid

| Declining Trend | Why |

|---|---|

| Neon / fluorescent colors | Oversaturated in 2023–24. Buyers are retreating to muted tones. |

| Gradient / ombré dye | High defect rate in production; consumers moved on. |

| Metallic yarn blends | Comfort complaints (scratchy). Durable only in low percentages (<5%). |

| Super-chunky (>5 GG) | High shipping cost per unit; limited wearing occasions. |

Sourcing Checklist for AW25/26

- Lock cashmere and alpaca yarn prices by June. Prices rise through Q3 as winter orders compete for limited supply.

- Order your core neutral colors (camel, oatmeal, navy) at higher MOQ for better pricing. These colors carry minimal sell-through risk.

- Test one differentiator color at low MOQ. If it sells, you have a signature color for your brand. If it doesn't, the exposure is limited.

- If using recycled fibers, verify GRS certification before placing the yarn order. Retroactive certification is expensive and slow.

- Specify the knit structure explicitly. "Rib" to one factory means 1×1; to another it means 2×2. Write the exact structure on the tech pack.

- Request a pre-production sample in the intended yarn and color, not a stock sample. A navy merino swatch from last season's dye lot will not match this season's dye lot.