Letter of Credit (L/C) Guide for Knitwear Buyers

Letter of Credit (L/C) Guide for Knitwear Buyers

You want to pay when goods arrive. The factory wants payment before shipping. Neither trusts the other. What solves this? A Letter of Credit.

An L/C is a bank-issued payment guarantee that protects both buyer and seller. The buyer's bank promises to pay the seller once shipping documents are presented. This guide explains how L/Cs work for knitted scarf and beanie orders — and how to avoid costly discrepancies.

1. What is a Letter of Credit?

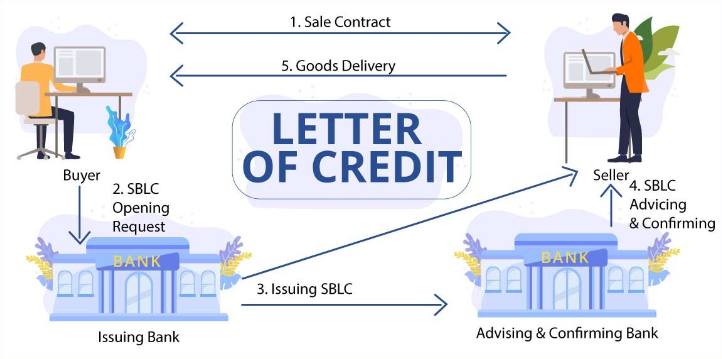

A Letter of Credit (L/C) is a bank's written commitment to pay the seller a specified amount, provided the seller presents compliant documents proving goods have been shipped.

- Buyer and seller agree on L/C terms in contract

- Buyer applies for L/C at their bank (issuing bank)

- Issuing bank sends L/C to seller's bank (advising bank)

- Seller ships goods and presents documents to their bank

- Bank checks documents and pays seller; buyer repays bank when goods arrive

Why use L/C?

- For buyers: Payment only released when seller proves shipment with correct documents

- For sellers: Bank guarantees payment if documents are correct, regardless of buyer's financial situation

2. Types of Letters of Credit

Irrevocable L/C

Meaning: Cannot be modified or canceled without all parties' consent. Standard for international trade.

Confirmed L/C

Meaning: A second bank (usually in seller's country) adds its guarantee. Protects seller if buyer's bank has credit risk.

Cost: Higher fees (confirmation charges 0.5-2% of L/C value).

When to use: Buyer's bank is in a country with political or economic instability.

Unconfirmed L/C

Meaning: Only the issuing bank guarantees payment. Most common for stable markets.

Revolving L/C

Meaning: Automatically renews for multiple shipments. Good for ongoing relationships with regular orders.

Transferable L/C

Meaning: Allows the seller to transfer payment rights to their supplier. Used when seller is a trading company.

3. L/C Costs (Who Pays What)

Buyer (Applicant) Costs

- L/C issuance fee: 0.1-0.5% of L/C value (minimum $100-300)

- Amendment fees: $50-150 per amendment if changes needed

- Bank charges: Cable fees, postage, handling ($50-200)

Seller (Beneficiary) Costs

- Advising fee: $50-200 (bank charges to receive and advise L/C)

- Confirmation fee: 0.5-2% (if confirmed L/C)

- Discrepancy fee: $50-150 per discrepancy if documents have errors

- Negotiation fee: 0.1-0.3% for document checking

For a $50,000 order, expect $250-1000 in total L/C fees split between buyer and seller.

4. Required Documents for Knitwear L/C

For a typical scarf or beanie shipment, these documents are required:

| Document | Description | Common Discrepancies |

|---|---|---|

Let me provide that table properly:

Required Documents

| Document | Description | Common Discrepancies |

|---|---|---|

I'll present the document list as text:

Required Documents for Knitwear L/C

- Commercial Invoice: Correct consignee, description matching L/C exactly, correct HS code, unit price and total value matching L/C

- Packing List: Carton numbers, quantities per carton, gross/net weight, carton dimensions

- Bill of Lading: Correct shipper and consignee, "on board" notation with date, clean (no clauses about damage), freight terms match L/C

- Certificate of Origin: If required by L/C, correct origin statement, issued by authorized chamber

- Insurance Policy: For CIF shipments, coverage amount (110% of invoice value), currency, risks covered

- Inspection Certificate: If L/C requires third-party inspection (SGS, Bureau Veritas, etc.)

5. Common L/C Discrepancies (and How to Avoid)

Discrepancies are errors in documents that make them non-compliant with L/C terms. Each discrepancy incurs fees ($50-150) and delays payment.

Most Frequent Discrepancies:

- Description mismatch: Invoice description does not match L/C wording exactly. Even extra spaces or punctuation cause rejection.

- Late shipment: Shipment date after L/C expiry or latest shipment date.

- Late presentation: Documents presented after L/C's specified period (typically 21 days after shipment).

- Bill of Lading issues: Missing "on board" notation, incorrect consignee, not "clean" (has clauses about damage).

- Amount mismatch: Invoice total different from L/C amount (partial shipment not allowed).

- Missing document: One required document not presented.

- Signature missing: Documents requiring signature not signed.

Even small typos ("Scarf" vs "SCARF") can be discrepancies. The bank checks documents literally, not commercially.

6. L/C Timeline for Knitwear Orders

- Week 1-2: Buyer applies for L/C at their bank (1-5 business days to issue)

- Week 2-3: L/C sent to seller's bank, seller reviews and accepts

- Week 3-10: Production happens (3-8 weeks)

- Week 10-11: Shipment, documents prepared

- Week 11: Seller presents documents to their bank (within 21 days of shipment)

- Week 11-12: Bank checks documents (3-7 business days)

- Week 12-13: Payment made to seller; buyer repays bank

7. L/C vs Other Payment Methods

| Method | Risk to Buyer | Risk to Seller | Cost | Best For |

|---|---|---|---|---|

Let me provide that comparison table clearly:

Payment Method Comparison

| Method | Risk to Buyer | Risk to Seller | Cost | Best For |

|---|---|---|---|---|

I'll present the comparison as text:

Payment Method Comparison

- TT (wire transfer) deposit + balance: Buyer pays 30% deposit, 70% before shipment. Buyer risk: medium (deposit lost if factory fails). Seller risk: low. Cost: $30-50 per transfer. Best for: Established relationships, orders under $20,000.

- L/C (Letter of Credit): Buyer risk: low (payment only on documents). Seller risk: low (bank guarantee). Cost: 0.5-2% of order value. Best for: Orders over $50,000, new relationships, large quantities.

- Open account (net 30/60/90): Buyer pays after receiving goods. Buyer risk: none. Seller risk: very high (no guarantee of payment). Cost: lowest. Best for: Long-term trusted relationships only.

- CAD (Cash Against Documents): Buyer pays when documents arrive at their bank. Buyer risk: medium (pays before seeing goods). Seller risk: medium (goods shipped but payment not guaranteed). Best for: Medium-sized orders, some trust established.

8. Red Flags in L/C Transactions

- L/C issued from a bank you don't know: Verify the issuing bank's reputation. Some countries have less reliable banking systems.

- Vague or overly complex terms: L/C with unclear requirements invites discrepancies.

- Unrealistically short shipment timeline: L/C requires shipment in 2 weeks when production takes 6 weeks — designed to force discrepancies.

- Soft clauses: Phrases like "documents acceptable to buyer" or "inspection by buyer" give buyer too much control — not truly irrevocable.

- Third-party documents required: Requirement for "inspection certificate by buyer" or "quality certificate by nominated person" can be used to block payment.

9. Buyer's Checklist for L/C

- ☐ Confirm L/C type (irrevocable, confirmed/unconfirmed)

- ☐ Verify issuing bank is reputable

- ☐ Check all dates (issue, shipment, expiry, presentation period)

- ☐ Ensure description matches contract exactly

- ☐ Confirm Incoterm matches contract (FOB, CIF, etc.)

- ☐ Check partial shipment and transshipment allowances

- ☐ Review document requirements (are they realistic?)

- ☐ Request draft L/C before final issuance to review

10. Questions to Ask About L/C

- ✓ "Do you accept L/C, or do you prefer TT?"

- ✓ "What L/C terms have you worked with before?"

- ✓ "Can you provide a sample of your invoice format?"

- ✓ "What discrepancies have caused problems for you in the past?"

- ✓ "Who pays for which L/C fees?"

Related Guide from Weave Essence

📘 Complete Sourcing Guide for Knitted Scarves & Beanies (L1)

Need help with L/C terms for your scarf or beanie order? Contact our team →